Yemen Economic Bulletin: Lebanon’s Financial Collapse Traps Yemeni Banks’ Money

In January 2020, demonstrators heckled a delegation of bankers leaving Lebanon’s central bank. This was not an uncommon occurrence – protests targeting the country’s political and financial elite had been ongoing for months. What was unique in this situation, however, was the identity of the banking delegation. These bankers were not Lebanese but Yemeni – not that the demonstrators were aware of this fact – and they had come to Beirut to inquire about hundreds of millions of US dollars worth of deposits stuck in Lebanese banks.

In January 2020, demonstrators heckled a delegation of bankers leaving Lebanon’s central bank. This was not an uncommon occurrence – protests targeting the country’s political and financial elite had been ongoing for months. What was unique in this situation, however, was the identity of the banking delegation. These bankers were not Lebanese but Yemeni – not that the demonstrators were aware of this fact – and they had come to Beirut to inquire about hundreds of millions of US dollars worth of deposits stuck in Lebanese banks.

During the ongoing conflict in Yemen, Lebanon emerged a vital clearinghouse to finance imports into the war-torn country. However, as Lebanon experiences its own slow-motion financial collapse today, the Yemeni economy, already in dire straits, is being placed under further strain.

Long before Dubai entered the scene, Lebanon was the region’s banking hub and Yemeni businesses have long used Beirut banks to store and transfer funds. Although the Lebanese banking sector is not as vibrant as it was in the 1950s, when it was a haven for Gulf oil money, until recently it was an attractive destination for regional money. Lebanon offered a dollarized economy, high interest rates and reputation for financial stability – Lebanese banks managed to not only survive but actually thrive during a 15-year civil war that ended in 1990, and chronic political deadlock since 2005.

Lebanon’s importance as a financial center for Yemeni businesses and banks grew in 2015 after the Financial Action Task Force (FATF), an intergovernmental body tasked with combatting global money laundering and terrorism financing, elevated Yemen’s risk designation to ‘high’.[1] Yemeni banks and businesses were already considered a risky proposition, after measures imposed on them in the years that followed the September 11, 2001, terror attacks on New York and Washington. The 2015 FATF designation led several banks in Western Europe and Canada to close correspondent accounts for Yemeni banks, and to end their relationships with major Yemeni businesses. While banks around the world sought to shed the risk of money tied to Yemen, Lebanese banks – most notably Bank of Beirut – remained willing to serve as a middleman, financing international trade to Yemen – in exchange, of course, for a sizable commission.

Several Yemeni banks had correspondent accounts in Lebanon’s banking system before the war, and the number has increased over the course of the conflict. The fact that Lebanese banks operated using US dollar accounts made it even more attractive for Yemen banks and clients – mainly traders and businessmen – since they didn’t have to pay additional currency conversion rates when making payments or foreign currency transfers (Yemeni importers and other essential trade service providers like shipping agents and brokers largely operate in dollars). Thus, there was an increased migration of Yemeni banks and business capital – most of it US dollars and Saudi riyals – to Lebanese banks. As of October 2019, Yemeni banks had the equivalent of US$240 million in foreign currency deposited in Lebanon, representing about 20 percent of total foreign currency deposits abroad at that time.[2]

No Money, More Problems

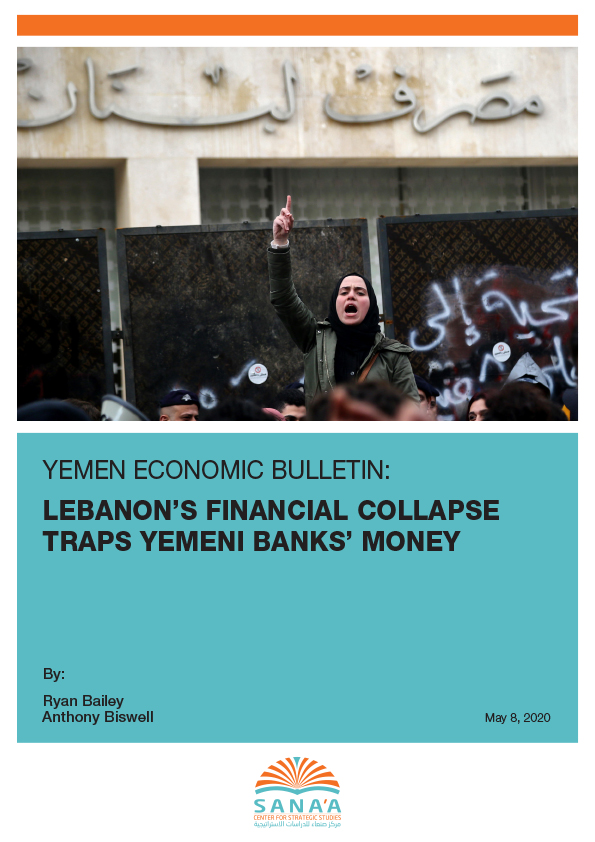

Yemeni banks’ exposure to Lebanon’s financial sector became clear in late October 2019 when popular protests against the deteriorating economic situation in Lebanon exposed the country’s financial house of cards. This collapse was the culmination of a number of factors, including: a perennial balance of payment deficit; high levels of government borrowing fueled mainly by mismanagement and corruption; years of falling foreign currency inflows; and, since 2015, an opaque ‘financial engineering’ mechanism whereby Lebanon’s central bank would offer obscene interest rates to local banks for depositing fresh dollars at Banque du Liban. After essentially inventing dollars that did not exist, banks were eventually no longer able to honor the $170 billion in deposits supposedly held by the financial sector.[3] The numbers in bank accounts no longer correspond to reality, a factor that has led to the description of the entire Lebanese banking system as a bonafide Ponzi scheme.[4] For all intents and purposes, Lebanon was broke.

Amid simultaneous political, debt, currency and banking crises, Lebanese banks introduced soft capital controls in November 2019, severely limiting withdrawals and banning transfers abroad. In March 2020, the country defaulted on its sovereign debt for the first time in its history.[5] Meanwhile, the local currency has lost more than 50 percent of its value in the parallel exchange market.[6] Yemen’s banks, just like ordinary Lebanese citizens, have found themselves unable to withdraw or transfer their money.

The inability of Yemeni banks to access their foreign currency holdings in Lebanon has diminished their essential role in facilitating the import of basic commodities into the country, a dangerous development given Yemen’s reliance on imports and the already dire humanitarian situation. The subsequent loss of confidence in Yemeni banks and traders whose money was suddenly, effectively frozen had immediate repercussions for shipments that were already in process and has cast doubt on future trade deals. Exporters withheld planned exports to Yemen until previous unpaid debts were honored. Roughly 30 Yemeni traders have had the experience of a Lebanese bank refusing to facilitate a transfer payment, a senior Yemeni banking official told the Sana’a Center on the condition of anonymity. Deals that had been secure or close to being secured were suddenly up in the air.

Confidence and trust are essentially unquantifiable. They are also essential ingredients for financial institutions and transactions. In the absence of both, problems soon arise and in the case of the Yemen economy spread quickly. The value of the Yemeni rial is intimately tied to the ability of the formal banking system to provide foreign currency to meet importers’ demand. Any amount of foreign currency that is suddenly frozen is significant, and could lead to a depreciation of the rial’s value in domestic exchange markets and with it the purchasing power of ordinary citizens.

Critics might say of Yemeni banks and their respective clients that “they knew the risks” for depositing foreign currency in Lebanon – a banking system offering obscene interest rates compared to the world average. But this ignores the severe financial constraints under which Yemeni banks and traders have been operating that made Lebanese banks a vital lifeline to ensure continued connectivity to formal regional and international banking networks.

The delegation of Yemeni banking officials that visited Lebanon at the beginning of 2020 engaged in near-daily negotiations with Bank of Beirut officials in an attempt to try and find a breakthrough to the current impasse. During their time in Beirut, the Yemeni delegation also presented its case to Lebanon’s central bank governor, Riad Salemeh. While the talks were cordial, no firm indication was given that the matter would be resolved anytime soon, and the delegation left empty-handed in the third week of February. One Lebanese economic analyst gave a damning assessment of the predicament that the Yemeni banks and businessmen find themselves in and their chances of breaking the deadlock, telling the Sana’a Center that the money may never be attainable, at least not without a sizeable “haircut”, meaning a reduction on the overall value of deposits.

Yemen’s Battle to Maintain Imports During War

Although some Yemeni banks have been more affected than others, developments in Lebanon represent yet another obstacle for the Yemeni banking system, importers and the country as a whole. While the majority of Yemenis do not use the formal banking system, critically Yemeni banks’ main clients are traders, specifically importers. In a country that imports up to 90 percent of its essential food commodities, everyone suffers from resultant shipment delays and price increases.

During the conflict Yemeni banks have been forced to find alternative ways of securing enough foreign currency to meet the demands of importers. Particularly after the suspension of hydrocarbon exports in 2015, the country’s main source of foreign currency, more pressure was put on the Central Bank of Yemen (CBY) to facilitate the import of essential commodities. The CBY had little choice but to dip into Yemen’s foreign currency reserves to preserve a letters of credit (LCs) system that was later reduced in scope to cover select food imports (after eliminating coverage for fuel and sugar). CBY also responded by limiting the ability of foreign currency account holders to withdraw funds as well as Yemeni banks’ ability to sell foreign currency to fuel importers. Despite the best efforts of then-CBY Governor Mohammed bin Humam and CBY staff, the letter of credit system became increasingly untenable as foreign currency reserves dwindled – from $4.7 billion in December 2014 to less than $1 billion in September 2016.

As the CBY struggled to maintain the value of the Yemeni rial and supply foreign currency, remittances took on an added importance in terms of facilitating imports. A number of Yemeni importers began to tap into informal financial networks, including the extensive hawala networks that bind Yemeni nationals in regional countries, specifically Saudi Arabia, to beneficiaries in Yemen. Remittance flows to Yemen pass through money exchange companies and informal hawala networks at a higher rate than through the formal banking system or international money transfer companies like Western Union. Tapping into these networks allows the importer to effectively join up the dots by connecting the increasingly isolated Yemeni importer to the foreign currency and bank account of external service providers including exporters and shipping agents.

Eventually, Saudi Arabia – the main backer of the Yemeni government and leader of the Arab military coalition – had to step in to shore up Yemen’s banking system and support the value of the rial. In November 2018, the government-backed Central Bank in Aden implemented a revised system for letters of credit underwritten by the $2 billion deposit Saudi Arabia provided in March 2018 to facilitate the import of five essential food commodities – rice, sugar, wheat, milk and cooking oil. Saudi Arabia also provided a $200 million cash injection in November 2018 to help the government stabilize the value of the Yemeni rial, which had depreciated from 215 Yemeni rials per US dollar in January 2015 to an unprecedented 800 Yemeni rials per US dollar in October 2018. Riyadh also provided $180 million worth of fuel (diesel and mazout) for electricity power generation in government-held areas from October 2018 to March 2019.

At the time of writing, Sana’a Center estimates that less than $200 million remains from the $2 billion. With the Saudi deposit almost depleted, it cannot be assumed that Riyadh will provide the same amount of financial support it has in recent years, not least because of the drop in global fuel prices and the economic impact of COVID-19.[7] As a result, the importance of the money frozen in Lebanon and the subsequent loss of confidence in Yemeni banks and importers is magnified.

The inability to access foreign currency deposited in Lebanon impacts Yemeni banks’ ability to facilitate the purchase of essential commodities that directly contribute to alleviating the humanitarian situation and famine in the country. This is a scandal – and one that should interest donor countries and institutions that gave some $3.6 billion to the Yemen Humanitarian Response Plan in 2019. The stakes are incredibly high, given the fact that 24 million Yemenis (80 percent of the population) are in need of some form of humanitarian assistance. Even as imports continue, the impact of importers needing to obtain foreign currency via informal financial networks at a higher exchange rate than they could with banks will be felt down the entire supply chain, resulting in higher prices for consumers.

Any missed and delayed payments for imports as a result of the Lebanese banking crisis – in particular Bank of Beirut’s liquidity issues and unwillingness to unlock funds – also constitute a longer-term threat to the international reputation of Yemeni banks and businesses. Yemeni bankers and merchants have expressed concerns over the loss of confidence in the ability of Yemeni banks and businesses to fulfill the terms of agreements through no fault of their own. This has already manifested itself in a reluctance by exporters and other key service providers such as shipping agencies to accept payments covered via letters of credit. Instead, they now insist on the resolution of unpaid balances before agreeing to future trade deals as well as requesting full advance payments for any future transactions. In a worst-case, albeit unlikely, scenario, international actors may refuse to conduct future banking transactions with Yemeni entities, leading to additional burdens on an already struggling economy and costs many times greater than the $240 million worth of foreign currency outstanding on Lebanese banks’ balance sheets.

Negotiation or Litigation

For Yemeni banks, immediate priority should be given to exploring avenues for unlocking deposits in Lebanese banks. Judging from the failed talks earlier this year between Yemeni and Lebanese banking officials, this will not be an easy task. Moreover, public opinion in Lebanon will likely be against any concessions for foreign depositors while Lebanese citizens cannot access their life savings and are falling deeper into poverty. At the same time, ordinary Yemenis should not suffer due to years of mismanagement and corruption in Lebanon. Thus, it seems there are three possible routes for Yemeni banks to take: negotiation, persuasion or litigation.

As a first step, another attempt should be made to negotiate the issue directly between Yemeni parties on one side and the Lebanese banks in question and the central bank on the other before any move is made to escalate the situation. Both sides would hopefully be willing to explore a compromise that would see at least a portion of the frozen funds released. While this may seem unfair to the Yemeni side, the ability to get something rather than nothing reflects the grim reality in place in Lebanon now. The country is in the midst of a deep recession[8] in which some depositors have resorted to withdrawing funds from trapped dollar accounts in Lebanese lira at the fixed exchange rate and converting them to dollars in the parallel market for less than 50 percent the “official” value.

If no agreement can be reached, it is more than likely that international pressure would need to be brought to bear on Bank of Beirut, Lebanon’s central bank and the Lebanese government to achieve a breakthrough. For the Yemeni side, potential allies include the World Bank, the International Monetary Fund (IMF) and the United Nations. As a point of leverage, the Lebanese government on May 1 officially requested billions from the IMF as part of a rescue package for the country.[9] Concessions related to Yemeni funds could be tied to any deal with the IMF. Major donor countries to Yemen could also plead the case for Yemeni banks through diplomatic channels with Lebanese authorities. These actors all have a stake in an outcome that empowers Yemenis to use their own money to import food and essential goods and promotes the use of the formal financial system in Yemen. In addition, a scenario where more trade is channeled through informal networks in order to access the foreign currency needed to complete deals, as opposed to the formal banking system, would increase the level of vulnerability to money laundering and terror financing, two principles that influenced the elevated risk categorization for Yemen and contributed to the migration of Yemeni deposits to the Lebanese banking system.

After exhausting all other avenues, Yemeni banks could decide to take legal action in an attempt to extract their deposits. There is precedent for such an approach. Oil trader IMMS filed a suit in a New York court in November 2019 against Lebanon’s BankMed over a $1 billion frozen deposit, and the two sides settled for an undisclosed amount in April.[10] [11] The fact that Lebanese banks use major American banks to facilitate dollar transactions makes them subject to US law. Still, the high costs and uncertainty of how much money, if any, Yemeni banks could gain after a drawn-out legal process favors less confrontational approaches.

Meanwhile, with Lebanon no longer an option, Yemeni banks must at the same time explore alternative destinations for correspondent accounts. Likely alternatives include the United Arab Emirates and Turkey, though these would entail currency conversion charges (either Emirati dirhams or Turkish lira to US dollars, or vice versa) for each transaction made. This unavoidable increased cost of doing business will be passed down to Yemeni consumers, further reducing purchasing power and increasing food insecurity.

The Yemen Economic Bulletin by the Sana’a Center serves as Yemen’s go-to economic newsletter, providing detailed analysis, commentaries, reactions and actionable recommendations.

The Sana’a Center for Strategic Studies is an independent think-tank that seeks to foster change through knowledge production with a focus on Yemen and the surrounding region. The Center’s publications and programs, offered in both Arabic and English, cover diplomatic, political, social, economic and security-related developments, aiming to impact policy locally, regionally, and internationally.

Endnotes

- “High risk and other monitored jurisdictions,” Financial Action Task Force, https://www.fatf-gafi.org/countries/#other-monitored-jurisdictions

- Information obtained by the Sana’a Center in November 2019.

- Jacob Boswall, “What’s next for Lebanon’s crisis-hit economy?,” Al Arabiya, November 28, 2019, https://english.alarabiya.net/en/business/economy/2019/11/28/What-s-next-for-Lebanon-s-crisis-hit-economy-

- Dan Azzi, “What is to be done,” An-Nahar, October 28, 2019, https://en.annahar.com/article/1057680-what-is-to-be-done

- “Lebanon to default on debt for first time amid financial crisis,” Agence France-Presse, March 7, 2019, https://www.theguardian.com/world/2020/mar/07/lebanon-to-default-on-debt-for-first-time-amid-financial-crisis

- A breakdown of the daily fluctuations in the exchange rate of the Lebanese lira against the US Dollar since November 2019 can be found here: lebaneselira.org

- Anthony Biswell, “Yemen’s Fate Hinges on the Economy,” The Sana’a Center for Strategic Studies, April 6, 2020, https://sanaacenter.org/publications/analysis/9601

- Timour Azhari, “‘Worse than the war’: Hunger grows in Lebanon along with anger,” Al Jazeera, April 19, 2020, https://www.aljazeera.com/ajimpact/war-hunger-grows-lebanon-anger-200417222253896.html

- Eric Knecht and Tom Arnold, “Lebanon banks reject rescue plan as government asks IMF for help,” Reuters, May 1, 2020, https://www.reuters.com/article/us-lebanon-crisis-plan/lebanon-banks-reject-rescue-plan-as-government-asks-imf-for-help-idUSKBN22D5NG

- Dmitry Zhdannikov and Eric Knecht, “Oil trader IMMS sues Lebanon’s BankMed for $1 billion: court filing,” Reuters, November 27, 2019, https://www.reuters.com/article/us-lebanon-bankmed-suit/oil-trader-imms-sues-lebanons-bankmed-for-1-billion-court-filing-idUSKBN1Y1284

- Matthew Amlot, “Lebanon’s BankMed and oil trader IMMS settle lawsuit,” Al Arabiya, April 12, 2020, https://english.alarabiya.net/en/business/economy/2020/04/12/Lebanon-s-BankMed-and-oil-trader-IMMS-settle-lawsuit

Chief Editor

Former Economic Analyst