Yemen Economic Bulletin:

The War for Monetary Control Enters a Dangerous New Phase

Executive Summary

Since September 2016, competing branches of the Central Bank of Yemen (CBY) have operated from either side of the frontlines in the country’s ongoing armed conflict, with the resultant fragmentation in monetary policy increasingly undermining domestic currency stability. Recently this has led to an accelerating collapse of the Yemeni rial-based currency system altogether and driven a migration toward the use of hard currencies – primarily Saudi riyals and United States dollars – for financial transactions inside the country.

From the internationally recognized Yemeni government’s interim capital of Aden, the central bank’s relocated headquarters has kept the institution’s international recognition, allowing it to, among other things, print currency and access international financial markets. Meanwhile, the central bank’s historic home in the capital, Sana’a, controlled by the Houthi group, has maintained its purview over the country’s largest consumer markets and financial centers.

The battle between the central banks entered a dangerous new phase on December 18, 2019, when the Sana’a branch banned newly-printed currency bills issued by its Aden rival and gave residents of Houthi-held areas a one-month window to trade in the “illegal” bills for either old ones – issued pre-September 2016 – or a new electronic currency the Houthi authorities are trying to implement. Turmoil has ensued.

This paper traces the beginnings of Yemen’s currency war and how monetary policy became fractured across frontlines. It examines the impacts of divided monetary supply management, as well as Houthi attempts to undermine Aden central bank policies and keep the country’s financial markets tethered to Sana’a. The Houthi decree in December 2019 marked a clear escalation in the currency war; this paper details the new banknote ban, how its enforcement has varied by region, as well as the e-Rial and its likely terminal flaws.

Market reaction to the banknote ban has seen flourishing black market currency trading, currency smuggling across frontlines, and the emergence of increasingly divergent exchange rates around the country as new rial banknotes have flooded back to government areas. In institutionalizing two monetary systems the Houthi move has had the political effect of furthering the emergence of distinct statelets within Yemen’s borders. In reaction to the ban, the Yemeni government has suspended public salary and pension payments to recipients in the north. The government is also dealing with dwindling foreign currency reserves, and some Yemeni economic observers suspect that the currency ban is a convenient pretext to stop payments amid looming liquidity issues.

Looking ahead, the broader implications of the currency ban include dangerous economic imbalances stemming from vast new impediments to business operations countrywide and commercial relocation out of Houthi-held areas. These, and the threat of rapid currency depreciation, have upped the pressure on the internationally recognized Yemeni government in its game of economic brinkmanship with the armed Houthi movement. It is ordinary Yemenis, however, who will continue to pay the heaviest price. A population in which millions already verge on starvation is set to bear increasing costs, further eroded purchasing power and a deterioration in the humanitarian situation resulting from the escalating currency war.

The Beginning of Yemen’s Currency War

Monetary Policy Fractures Across Frontlines

The armed Houthi movement took over the Yemeni capital, Sana’a, in September 2014, and by March the following year the group and its allies had pursued a military campaign all the way to the southern port city of Aden, prompting a regional military intervention led by Saudi Arabia and the United Arab Emirates. Aden and much of southern Yemen was liberated through the summer of 2015, establishing rough north-south frontlines that have largely persisted until today.

The onset of war led to general economic collapse across Yemen. In parallel, eroding faith in the country’s banking system induced wealthy Yemenis and traders to withdraw their cash and circulate it in the informal markets. In the first six months of 2016 alone some 300 billion Yemeni rials (YR) left the banking system.[1] The banks’ subsequent shortage of physical Yemeni rials (YR) meant they had none to deposit at the Central Bank of Yemen (CBY) in Sana’a. The internationally recognized Yemeni government, which established an interim capital in the southern city of Aden following the city’s liberation, had maintained a degree of authority over the CBY and barred the central bank from printing more cash. Consequently, by August 2016, the CBY was forced to suspend salary payments to civil servants countrywide, given that it did not have the physical cash with which to pay them.

Meanwhile, oil exports had also been suspended in 2015, cutting the country off from what had been its largest source of foreign currency. Yemen is overwhelmingly dependent on imports for food, fuel and other basic commodities, and the need to continue financing these imports depleted the CBY’s foreign currency reserves, which fell from US$4.6 billion at the end of 2014 to US$700 million by September 2016.[2]

On September 18, 2016, President Abdo Rabbu Mansour Hadi, head of the Yemeni government, ordered the CBY headquarters to be moved from Sana’a to Aden. This move fractured the institution across the conflict’s frontlines and left both branches with severely reduced institutional capacity. The new Aden-based central bank took with it the CBY’s international recognition, and thus the right to access global financial systems and international support, and to print new currency. The Sana’a-based branch continued to operate under Houthi control, having kept the vast majority of the central bank’s staff, informational archives and purview over Houthi-held areas, which include the country’s largest population centers, commercial markets, and business and financial hubs. The differing features of the divided central bank branches have formed the respective leverage points each has employed against the other in their increasingly acrimonious struggle for dominance. In the years since the split, the two CBY branches have fought over the ability to regulate the money supply, import financing, banks and money exchangers, while cohesive, countrywide monetary, fiscal and economic policy became impossible for either to implement.

The Yemeni Government’s Expansionary Monetary Policy

In January 2017, the Aden-based central bank received its first order of new Yemeni rial banknotes – worth YR200 billion – from the Russian company Goznak. The Yemeni government, no longer receiving oil receipts and consequently facing a massive public budget deficit, aimed to pay its bills through having its central bank print the cash it needed. The new money was also intended to replace damaged and deteriorating banknotes already in circulation, many of which were printed on poor quality paper and had an estimated useful lifespan of two years. This expansionary monetary policy continued in the years following, with the World Bank noting a “massive issuance of new banknotes” in 2018 that saw the money supply increase by 53 percent.[3] By the end of 2019, the Aden central bank had printed YR1.7 trillion worth of new bills, according to a senior Yemeni banking official, of which roughly YR200 billion is currently held in reserve.

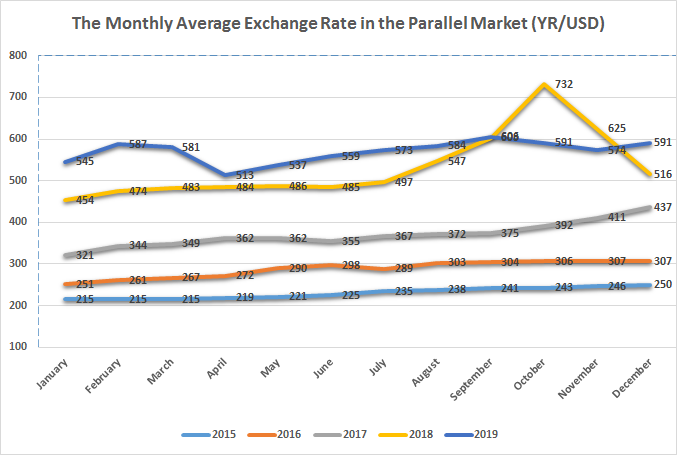

Limited foreign currency availability and increased domestic currency supply consequently led to exchange rate instability and downward pressure on the value of the Yemeni rial. In 2014, the local exchange rate was YR215 per US$1; by the end of 2018 it was YR516 per US$1. In one of the world’s poorest and import-dependant countries, such loss in purchasing power has had profound humanitarian implications.[4]

Source: Central Bank of Yemen, World Food Programme, and Sanaa Center Economic Unit

The Houthi Response

In June 2017, the Houthi-led National Salvation Government responded by calling for the new Aden-issued YR500 banknote to be prohibited from circulating in Houthi-controlled areas. There were several intersecting motivations for this. Publicly, the authorities in Sana’a said they aimed to mitigate the inflationary impacts of the Yemeni government’s expansionary monetary policy. The Houthi authorities also wanted to protect their control over the country’s largest currency market, in Sana’a – if the Aden-issued rial banknotes were permitted in Houthi areas they could be used to purchase, and drain, the foreign currency from Sana’a to Aden. Asserting some degree of control over the money market would help keep the country’s banking and financial systems tethered to Sana’a and undermine the credibility and effectiveness of the Aden central bank.

Between June 2017 and June 2018, the Houthi authorities held several meetings with Yemeni banks and money exchange outlets – the majority of which are headquartered in Sana’a – to repeatedly instruct them not to trade in the newly printed currencies. In June 2018, the Houthi-based Ministry of Industry and Trade issued a circular to the Chamber of Commerce and Industry obliging importers, wholesalers, malls and oil derivatives stations in Houthi areas not to deal with the new YR500 and YR1,000 denominations issued by Aden central bank. Inspection and follow-up campaigns intensified in 2019, with the Sana’a-based CBY coordinating with security agencies and the public prosecutor’s office to ensure that markets, shops, restaurants and financial institutions did not accept new banknotes of any denomination. As of mid-December 2019, Houthi seizures of banned bills had resulted in the confiscation of more than YR600 million in currency issued by the Aden central bank, according to a Sana’a-based banking official.

The Houthi ban on the new banknotes helped limit the overall rial supply in Houthi-held areas relative to Yemeni government areas, resulting in differing YR-foreign currency exchange rates between northern and southern Yemen. From 2018 through mid-December 2019, this differential had generally ranged between YR5 and YR15, with the rial being worth slightly more in Houthi-controlled areas. The Houthi restrictions against new banknotes printed in Aden were not uniformly enforced, however. Above all, their focus was Yemeni banks, which were instructed to set aside newly-printed rials they came across for collection by the Houthi-run National Security Bureau (NSB).[5] A portion of these banknotes was flushed out of Houthi-controlled territory to government-controlled areas through the purchase of fuel and cooking gas from government-held Marib governorate, according to a Sana’a-based banking source. The somewhat discretionary application of the ban allowed space for some newly-printed banknotes to enter into regular circulation for normal day-to-day transactions. According to independent banking sources, Aden-issued cash circulating in Houthi-controlled areas was estimated at YR300-350 billion, or roughly a quarter of all rial bills changing hands in northern areas.

Houthis Escalate the Currency War

The Blanket Banknote Ban and Promotion of the e-Rial

On December 18, 2019, the Sana’a central bank issued a directive that formally prohibited the use in Houthi-controlled territories of new Yemeni rial banknotes issued in Aden. The circular ordered those in Houthi-held areas to hand over any “illegal” notes in exchange for either electronic currency or physical banknotes printed before September 2016. The directive gave residents in Houthi areas a 30-day window to exchange their banned banknotes, which ended on January 17, 2020. Those caught with outlawed bills following the grace period now face the money being confiscated and possible imprisonment. The decree thus expanded the scope of previous prohibitions against Aden-issued bills – to include now businesses and individuals – while also making the penalties more severe.

The Sana’a central bank specified three service providers where “illegal” banknotes could be swapped for the electronic currency, or ‘e-Rial’: M Floos (owned by Al Kuraimi Islamic Microfinance Bank); Mobile Money (owned by Cooperative & Agricultural Credit Bank); and Quality Connect (jointly owned by Yemen Kuwait Bank, Swaid & Sons for Exchange, and Al Akwaa Exchange). Other select banks and money exchangers were also accepting trade-ins of newly-printed banknotes for an equivalent amount of e-Rials. Yemenis without accounts at approved financial service providers could receive in-kind transfers (phone credit) to their mobile numbers instead of e-Rials. Although individuals could also exchange new currency for old bills at these official locations, the trade-in amount was capped at 100,000 Yemeni rials. The Houthi authorities also announced that previously confiscated new currency bills would be converted into e-Rials.

The issuing of electronic currency is not the Houthi authorities’ first attempt at expanding their liquidity options while decoupling from Aden-issued bills. In April 2017, Houthi authorities introduced a voucher system to cover basic foodstuffs for public sector employees who were not receiving salaries due to a lack of banknotes with which to pay them. The scheme began to crack when the authorities could not pay merchants attempting to redeem the vouchers for cash with which to restock inventory. This quickly resulted in a depreciation in the value of the coupons and a two-tiered price system for consumers: one for cash payments and another for vouchers.[6] The coupon system ultimately failed.

The Houthi authorities tested an electronic currency system in March 2018, and then in April 2019 rolled out a larger pilot program to pay employees at the Houthi-run Yemen Petroleum Company (YPC) in e-Rials.[7] The YPC was selected after other state-run institutions – such as the Yemeni Telecommunications Corporation – objected to the idea of incorporating e-payments, although YPC employees in Sana’a also organized demonstrations to protest the plan. Nine months on, the e-Rial can still only be used to pay limited expenses, such as water and electricity utility bills and mobile phone services. There is currently no mechanism for using the e-Rial for normal daily economic activities. Even if one were implemented, merchants would almost certainly face difficulties exchanging e-Rials for hard currency to purchase imports and restock inventory, for reasons similar to the fatal flaw in the coupon scheme. Another inherent challenge to electronic currency adoption is that Yemen is a heavily cash-based economy – before the current conflict only 6 percent of Yemenis held bank accounts, according to CBY data. The e-Rial’s viability is thus highly uncertain, if not already predestined for failure.

In Practice, Enforcement Varies by Region

The Houthi authorities’ enforcement of the ban has varied by region, with the most observable response to the new directive in Sana’a and surrounding governorates. In other Houthi-controlled areas, particularly in governorates near or containing government-held territory, the continued circulation of newly-printed banknotes is more common, according to banking officials who spoke with the Sana’a Center.

In the more-densely populated Houthi regions businesses are facing a shrinking money supply and a lack of physical liquidity in a heavily cash-based economy. In Sana’a, where most banks, businesses, money exchangers, state institutions and economic infrastructure are based, local businesses are no longer accepting new banknotes. Residents in the capital are increasingly unable to carry out basic and essential financial transactions, such as purchasing food, fuel and medicine. According to sources in Sana’a, even qat dealers – visited by millions of Yemenis daily for the plant shoots they sell with mild stimulant properties – no longer accept Aden-issued currency. A similar case exists in neighboring Houthi-controlled governorates such as Dhamar, where new rial notes are no longer accepted for basic transactions at shops, businesses and financial service providers.

In governorates divided between Houthi and government control or near active frontlines, there is a larger supply of the newly-printed banknotes that are still being used, and in wide circulation compared to Sana’a, according to a senior banking official. This includes the governorates of Ibb, Taiz, Al-Dhalea, Hudaydah and Al-Jawf. For example, in Ibb, new banknotes represent 60 to 70 percent of the total currency circulating in the governorate. Accounting for this reality, Houthi authorities have not yet enforced a total ban on the circulation of new banknotes in these frontline areas and Houthi fighters stationed there have been granted waivers from the directive.

Market Reaction: Illicit Trading and Multiple Exchange Rates

Across Houthi-controlled areas there have been varying degrees of engagement and compliance with the new banknote ban. Yemenis generally appeared reluctant to hand over physical, newly-printed banknotes in their possession to designated agents in exchange for electronic currency. A senior banking official estimates that less than 10 percent of the new banknotes in Houthi areas were turned over at the officially designated outlets by January 17.

Given the individual cap of YR100,000 on trading in new bills at official outlets, anecdotal evidence suggests many people resorted to the black market, where traders were exchanging new banknotes for old ones, however not for equivalent value. In Hudaydah governorate, for example, YR10,000 in new banknotes were being exchanged for YR9,000 in old currency bills, according to UN agencies, representing a 10 percent differential. The price discrepancy between old and new rials was also apparent in government-controlled areas: in Al-Dhalea governorate traders reported that goods were being valued according to the currency they were purchased in, with old banknotes worth 1.10 to 1.12 times more than new bills. Further complicating the situation, roughly 90 percent of the old, pre-2016 banknotes in circulation today are damaged and technically unfit for circulation, according to a senior banking official. Should the ban on new bills be prolonged, fees for exchanging rial banknotes will inevitably increase as old bills become completely unusable, leave circulation and decrease supply.

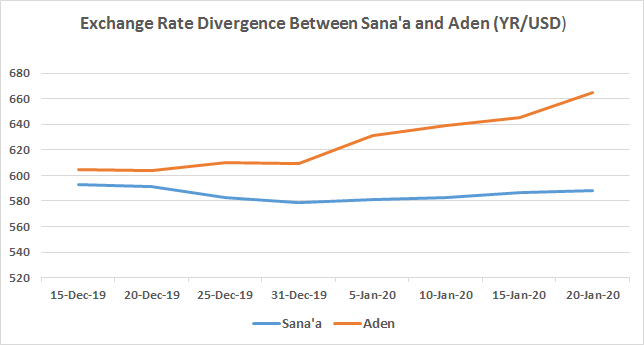

Different pricing for new versus old rial notes has created increasingly divergent exchange rates for converting rials into foreign currency between Houthi and government-controlled areas. On December 31, 2019, the exchange rate was hovering at YR582 per US$1 in Sana’a compared to YR 612 per US$1 in Aden, a difference of around 5 percent. The increased movement of new rial liquidity away from Sana’a to Aden widened this divergence, and on January 14, 2020, the exchange rate in Aden jumped to YR655 per $1 compared to YR590 per $1 in Sana’a, an 11 percent difference. In response, money exchangers have substantially increased fees for domestic money transfers from government to Houthi-controlled areas – from less than 1 percent pre-directive to roughly 12 percent as of mid-January, according to money exchangers in Sana’a and Aden who spoke with the Sana’a Center.

Source: Sana’a Center Economic Unit

There are various current determinants of a rial’s value: whether it is traded in Houthi- or Yemeni government-controlled areas, and whether that rial is an old bill, new bill, or exists physically at all. The latter is due to the distinction made between bank accounts opened before the conflict where money can only be withdrawn in the form of a check vs. accounts opened during the conflict that can withdraw cash. Further divergences in pricing between different cash and non-cash payment instruments can be expected if the ban on Aden-printed banknotes continues and the planned electronic currency scheme payment comes into operation. This would likely lead to a divergent value for e-Rials vs. physical notes, given the former’s limited utility for daily purchases. In the continued absence of a unified foreign exchange system, the rial would be increasingly vulnerable to pressure shocks and the resultant price volatility.

The new market conditions have increased the profit potential from currency arbitrage, and currency smuggling across frontlines has increased. For example, foreign currency purchased in Houthi-held territory can be sold in government-held territory for a profit. Independent banking sources reported that Houthi-aligned smuggling networks have been encouraged to bring old banknotes from government-held areas as part of a concerted effort by the authorities in Sana’a to accumulate larger physical currency reserves.

The Response from Aden

In response to the Houthi directive, the Aden central bank issued a statement on December 22 dismissing the authority of the Sana’a central bank and insisting on full adherence to the monetary and fiscal policies of the internationally recognized Yemeni government. The statement urged banks, businesses and money exchange companies to continue using Yemeni rial banknotes issued after September 2016. Importantly, the Aden central bank also restricted the country’s commercial banks from issuing more than 15 percent of their total capital in e-Rial, which would cap the potential for e-Rial issuances at YR5 billion, according to a senior banking official.

On December 30, the Yemeni government’s Ministry of Finance issued another statement announcing that it would be unable to transfer funds for the payment of public sector employees and pensioners in Houthi-controlled areas because banks and money exchange firms had refused to receive new bills. As mentioned above, since late 2016 the country’s liquidity crisis has prevented many of Yemen’s estimated 1.25 million public sector employees from receiving regular, full salary payments. However, some workers in health, judiciary and higher education sectors, along with some 40,000 pensioners,[8] have been receiving approximately YR12 billion collectively on a monthly basis from the Yemeni government over the last three years.

The Yemeni government normally made these transfers through Al Kuraimi Islamic Microfinance Bank. A Sana’a-based banking official appraised of the situation said that the Yemeni government needed to secure the old rial bills necessary for distribution in northern areas, as Al Kuraimi was unable to. He added that the government had halted transfers to northern areas on December 18, the same day the Houthi authorities announced the currency ban. An Aden-based banking sector official noted that, as with money transfers to northern areas generally in the current environment, the Yemeni government would face a 10 percent fee on any salaries and pension payments it sent to recipients in Houthi-held areas.

Several sources within the Yemeni banking sector who spoke with the Sana’a Center suggested the Yemeni government is facing its own liquidity issues related to the $2 billion Saudi deposit – which Riyadh gave to the Aden central bank in 2018 to facilitate import financing and support the Yemeni currency – being almost exhausted. In that case, the Houthi decree would be a timely pretext for ending the payments in northern areas.

Looking Ahead

Economic Stagnation, Commercial Relocation and Impediments to Business

If Houthi authorities hold firm to their ban on Aden-issued currency circulating in northern areas, such a campaign could cause major downturns in economic and business performance for the entire country. For one, any further removal of banknotes from circulation in northern areas would radically shrink the monetary supply base, with the effect of limiting consumer capacity to bridge the gap in YR-US$ value lost since the conflict began. Put differently, if an item in 2014 cost YR4,000, it would today cost at least YR10,000, according to average price inflation. Local currency in circulation has to grow in size to compensate for this loss in consumer purchasing power, lest economic stagnation set in. As is, reduced monetary supply in Houthi controlled areas has almost certainly contributed to the decline in commercial sales since December, as noted by a Sana’a-based banker. Given that Houthi-held areas represent the largest consumer markets, stagnation there would impact commerce countrywide. The Houthi ban on Aden-issued currency undermines the necessary replacement of more than YR1 trillion in damaged or destroyed old notes currently circulating in the economy. Small-denomination old banknotes (YR100 and YR200) have also become rare in Houthi-controlled areas as many issued prior to 2017 have become so damaged that they are unusable. This has become a major obstacle to carrying out small day-to-day purchases.

The Yemeni economy, in both Houthi and government-controlled areas, relies heavily on imports, and major importers based in Houthi areas distribute commodities across the entire country. However, trade between Houthi and government territory is becoming more challenging, risky and expensive due to the divided currency regimes. Anecdotal evidence suggests there has already been some relocation of commercial activities from Houthi-controlled areas to government-controlled territories. Previously, traders and importers would hold their inventory of goods in Sana’a and from there distribute them to other areas. Recently, however, some traders have begun instead to stockpile goods in Aden or Marib governorates and distribute them from there to Sana’a and other Houthi-controlled areas. This allows merchants to avoid additional costs resulting from the Houthi directive – such as securing old rial notes or transferring liquidity between government and Houthi-controlled areas.

As the currency war has escalated, traders and commercial actors in Houthi-controlled areas have sought other mechanisms to avoid punishment and the risk of their money being confiscated. According to sources working at money exchangers, some traders have begun buying gold or other goods from southern, government-controlled areas with new rials to then sell them in Houthi-controlled areas in exchange for the permitted old currency. This effectively allows them to exchange Aden-issued bills for old banknotes without incurring the 10 percent, or more, commission the black market would charge. Other traders are increasingly using hard currencies – Saudi riyals and US dollars – to conduct financial transactions and exchange goods across frontlines.

Threat of Rapid Currency Depreciation Ups Pressure on the Yemeni Government

In southern areas, as mentioned, the new influx of currency is already having significant inflationary impacts and creating a diverging rial exchange rate relative to northern areas. Since the currency schism started in mid-December 2019, the rial has depreciated from around YR580 to more than YR650 against $US1 in government-held areas as large amounts of Aden-issued new physical liquidity have flowed out of Houthi-controlled territories. Government-controlled areas are less densely populated and are host to significantly less daily economic activity than Houthi-held areas, meaning new rials in circulation there have a relatively greater inflationary impact.

This comes at the same time that the Aden central bank is also under threat of exhausting its foreign currency reserves. Since 2018, Saudi Arabia has provided the Aden central bank with roughly US$2.4 billion in foreign currency support: a US$2 billion deposit for the CBY to underwrite essential imports and $380 million in foreign currency and fuel grants to support power generation. In mid-2019 the central bank in Aden also reached an agreement with the Saudi government to channel some 370 million Saudi riyals (nearly US$100 million) over the Aden-based CBY terminal system monthly. This amount had previously been paid directly to local forces fighting on behalf of the Yemeni government.[9] As of the beginning of 2020, however, the Aden-based CBY had only US$3oo million foreign currency holdings remaining.

Protecting the domestic currency against the deflation pressures it currently faces would likely require the Aden central bank to exhaust its remaining foreign currency reserves before the end of the first quarter of this year, according to a senior banking official. Given the current foreign currency holdings available to the Aden CBY and the increased currency instability the intensifying war between the central banks has wrought, the Yemeni rial is under imminent threat of experiencing further rapid depreciation.

The Houthi directive to ban the Aden-issued rials – with the predictable panic and negative economic repercussions it has instigated in Yemen – was likely timed to exert maximum pressure on the Aden central bank to ease off on policies that are undermining Houthi economic interests. Upping the stakes gives the Houthis leverage to extract concessions in various areas, such as the ongoing UN-led negotiations over the implementation of the government’s Decree 49 regulating fuel imports. While fuel importers having been paying import taxes and customs fees into a special account at the Hudaydah central bank branch, an agreement is yet to be reached over which public sector employees in Houthi-controlled territories will receive their monthly salaries from these funds. The government insists on payments being made to only those registered on the public sector payroll as of 2014, while the Houthis want this to be expanded to include those hired since they seized control.

Impact on Lives, Livelihoods and the Humanitarian Effort

Already some 24 million people in Yemen – 80 percent of the population – are in need of humanitarian assistance, of which 7.4 million at risk of famine. Humanitarian actors trying to address these needs will face severe new obstacles under the currency ban. Large portions of the multi-billion dollar aid relief in Yemen is distributed as cash transfers using the new Aden-issued currency notes – which are no longer accepted in northern areas where most aid recipients are located. To distribute funds in the north, aid agencies will face increased fees, and thus each aid dollar will have a diluted impact. Meanwhile, thousands of public sector employees and pensioners in northern areas have also lost their salaries following the Yemeni government’s December announcement that it was suspending payments, although the rationale behind the government’s decision remains unclear.

Hundreds of thousands of Yemenis have also departed Houthi areas in search of income opportunities in government-controlled areas. For instance, the population in Marib has increased from roughly 300,000 pre-conflict to more than 2 million today. Many of these people have families remaining in Houthi areas that rely on remittances for survival. The currency ban has impeded their ability to transfer these funds. As noted above, a fee of at least 10 percent is now common for money transfers from government to Houthi areas and for currency exchanges from new to old rials.

Thus, looking ahead, ordinary Yemenis will remain the ultimate victims if this currency war continues, as their costs rise, their money loses value and their economy comes apart.

*Editor’s Note: A previous version of this article stated that Al Kuraimi Islamic Microfinance Bank had requested a fee from the Yemeni government to transfer public salary and pension payments to recipients in Houthi-held areas. Al Kuraimi in fact did not make such a request. The Sana’a Center apologizes for the error.

Report edited by Ryan Bailey and Spencer Osberg.

The Yemen Economic Bulletin by the Sana’a Center serves as Yemen’s go-to economic newsletter, providing detailed analysis, commentaries, reactions and actionable recommendations.

The Sana’a Center for Strategic Studies is an independent think-tank that seeks to foster change through knowledge production with a focus on Yemen and the surrounding region. The Center’s publications and programs, offered in both Arabic and English, cover diplomatic, political, social, economic and security-related developments, aiming to impact policy locally, regionally, and internationally.

Endnotes

- Mansour Rageh, Amal Nasser and Farea al-Muslimi, “Yemen Without a Functioning Central Bank: The Loss of Basic Economic Stabilization and Accelerating Famine,” Sana’a Center for Strategic Studies, November 2, 2016, https://sanaacenter.org/publications/main-publications/55

- Ibid.

- “Yemen Economic Monitoring Report,” World Bank Group, Winter 2019, p.8, http://documents.worldbank.org/curated/en/161721552490437049/pdf/135266-YemEconDevBrief-Winter-2019-English-12-Mar-19.pdf

- “Yemen: 2019 Humanitarian Needs Overview [EN/AR],” UN OCHA via Reliefweb, February 14, 2019, https://reliefweb.int/report/yemen/yemen-2019-humanitarian-needs-overview-enar

- With the exception of the National Bank of Yemen and the rival Cooperative & Agricultural Credit Bank (CAC Bank) established in November 2018, the remaining 17 banks currently operating in Sana’a are also headquartered in the capital.

- “‘Food vouchers issued’ Yemen at the UN, April 2017,” Sana’a Center for Strategic Studies, May 8, 2017, https://sanaacenter.org/publications/yemen-at-the-un/99

- “‘Houthi Authorities Attempt an Electronic Rial Payment System, Again’ Game of Parliaments – The Yemen Review, April 2019,” Sana’a Center for Strategic Studies, May 7, 2019, https://sanaacenter.org/publications/the-yemen-review/7357#Houthi-Authorities-Attempt-

- Public servants receiving salary payments from Aden include employees working in non-military and security institutions such as the judiciary, the Central Organization of Control and Audit (COCA), the General Authority of Insurance and Pension, public universities and the public health sector. The Yemeni government has also disbursed some salary payments to public sector workers in frontline areas in Hudaydah, Al-Dhalea, Al-Bayda and Taiz governorates.

- The central bank in Aden has been using this regular foreign currency influx to cover the import of all food commodities at the preferential exchange rate of YR 570 to 1 USD. On the other hand, oil derivatives are covered using a mediated exchange rate 10 percent lower than the exchange rate prevailing in the parallel market.

- “Yemen: 2019 Humanitarian Needs Overview [EN/AR],” UN OCHA via Reliefweb, February 14, 2019, https://reliefweb.int/report/yemen/yemen-2019-humanitarian-needs-overview-enar

Former Economic Analyst

Chief Economist